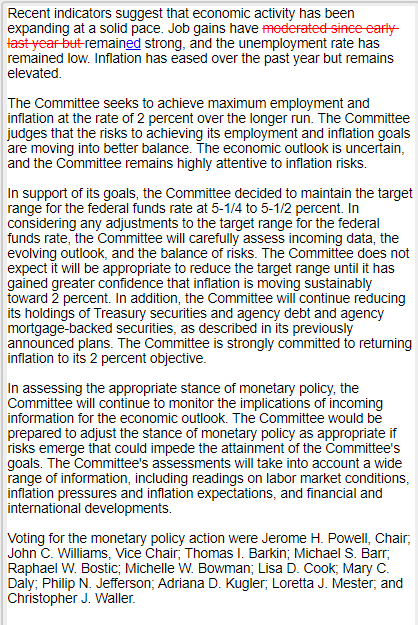

Last week we had the latest FOMC meeting and although rates were once again unchanged, we received a plethora of updates in terms of monetary policy thinking.

Alongside no change in Fed Funds Rate, the statement itself saw very few changes as well:

Much of the market moving information from the FOMC meeting was in relation to future guidance around when rate cuts will begin, and how many are expected.

Due to a few hotter-than-expected inflation prints in recent months, many went into the meeting expecting the FOMC to have a hawkish tone and to walk back the potential of rate cuts occurring this year due to inflation accelerating again in recent months.

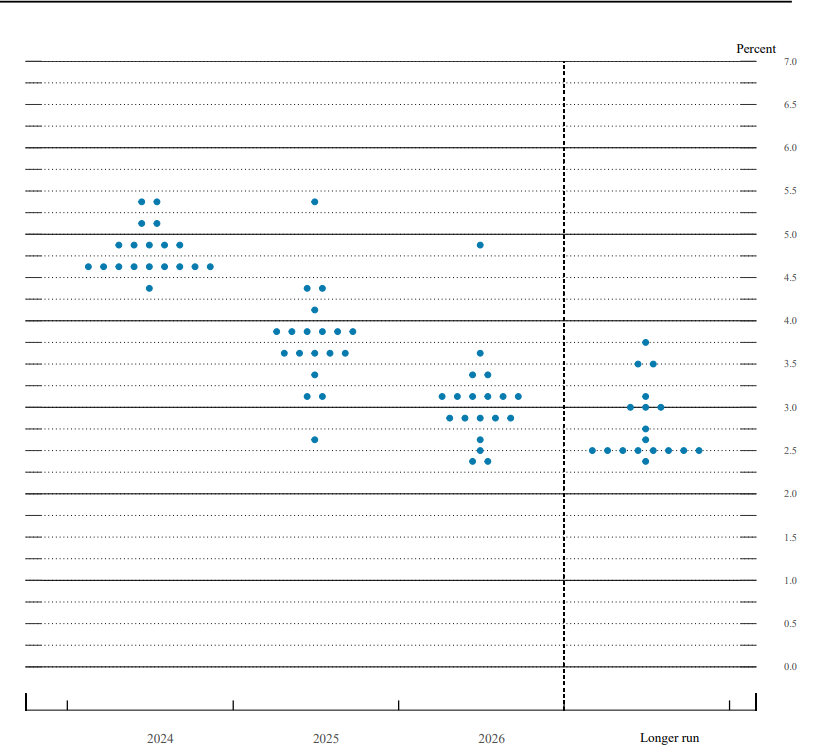

With the release of the new dot plots, however, we see that nothing has changed the Fed’s view enough to walk back their guidance to rate cuts starting this year:

Overall, we have a few takeaways:

- The Fed sees no change in its plan to have a median 3 rate cuts in 2024, with the first cut most likely starting in June

- There are continued forecasted rate cuts in 2025 and 2026 that setup the plan for the Fed Funds Rate to return to around 2% in line with their inflation goal

- One interesting note is a slight uptick in the Fed’s longer run rate expectations. Whereas before the median was 2.5% we saw it increase to 2.6%. Though this is a small change, it could also hint at the potential for the Fed to be rethinking what a potential inflation target could be in the future and increasing it from the 2% level.

Overall, the message from the Fed was that they are not making decisions at the whim of 1-2 datapoints such as a couple of CPI prints. The reaction function is based on a much more holistic and complex decision process and overall they are not really looking for “better” inflation data, but just continued “decent” data.

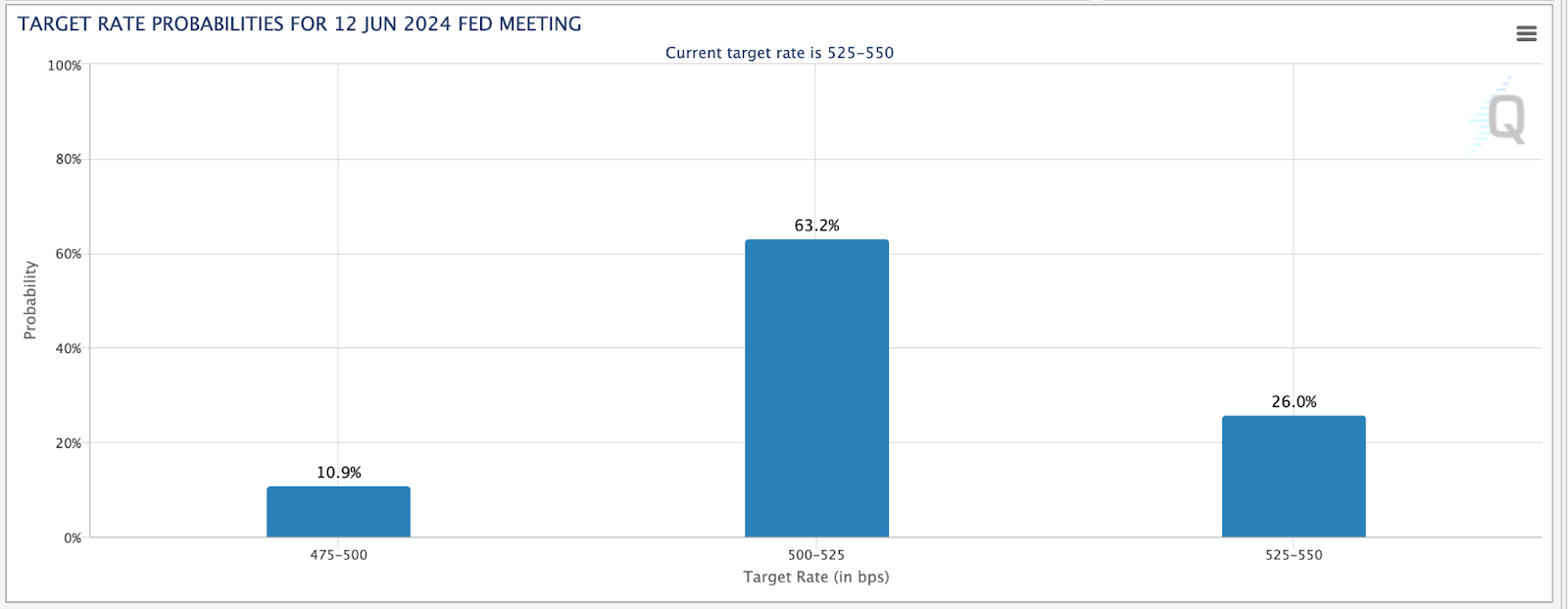

Following this and the FOMC press conference, we now see a 63% chance of a rate cut in June:

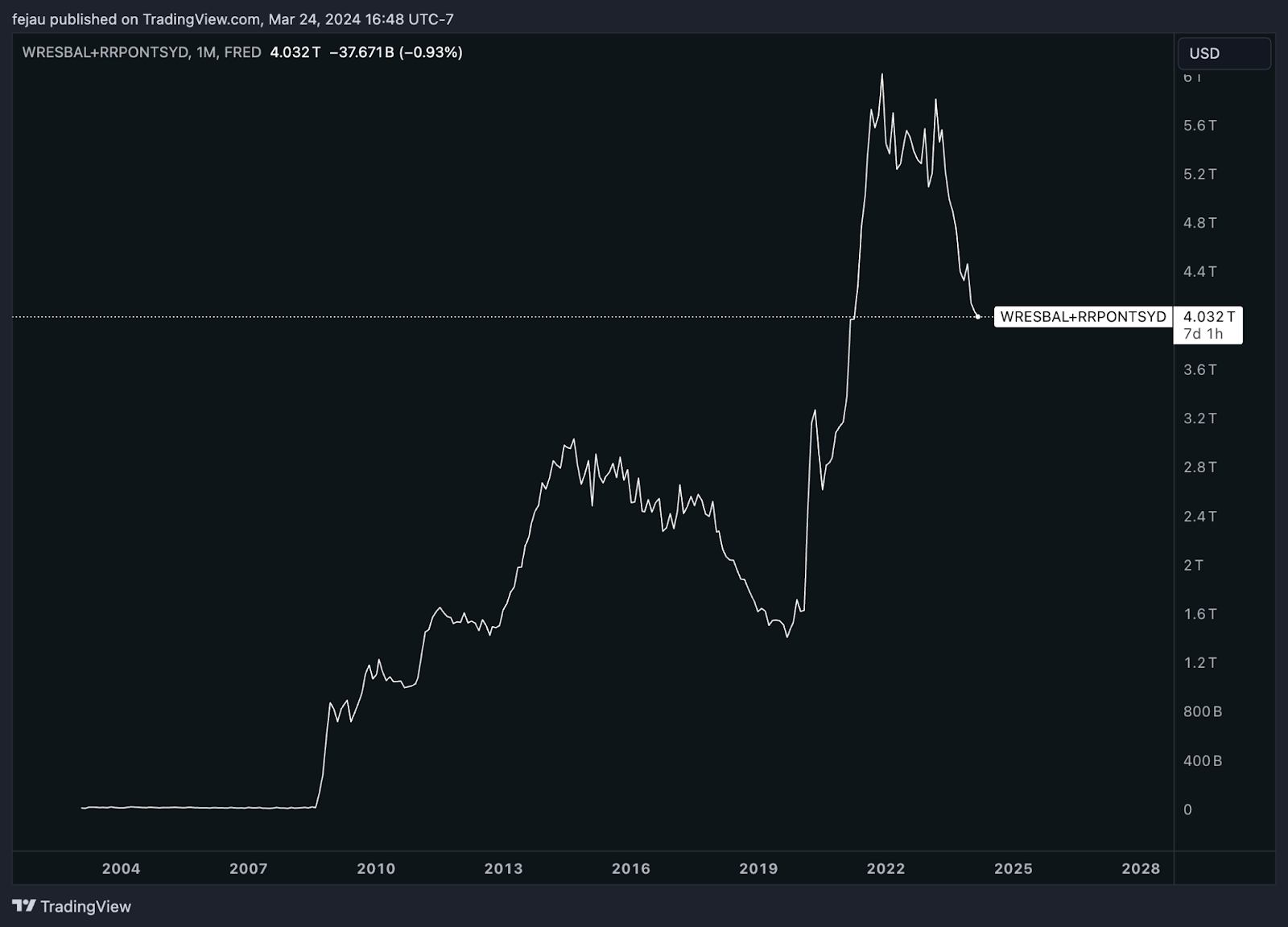

One other major insight we received was an update around Quantitative Tightening and the plan for tapering the program.

Importantly, the Fed views total reserves as the aggregate of both bank reserves + RRP balance.

Adding the two together, we get this chart:

During the press conference, Chair Powell mentioned that QT taper plans were discussed at the meeting and it will begin “soon”. Soon, in central bank speak is about as guaranteed as it gets in terms of something occurring. Although we will learn more once the FOMC minutes come out next month, Powell provided a few hints that give us an idea of what could be coming:

- A formal announcement of the QT taper plan will come at the next meeting in May.

- Most likely, this will set the stage for the QT taper to begin at the following meeting in June, in line with the potential first rate cut of the cycle.

- Powell emphasized that they want to slow down QT because they do not want a repeat of September 2019, where the last time QT was occurring we saw the overnight repo market blow up and the Fed have to stop QT overnight and provide repo liquidity. Due to the fact that there is a standing repo facility now and that the Fed is already slowing down QT at a time where there is still “abundant” reserves, we most likely will not see any money market fireworks like last time.

- Considering that the Fed wants their MBS book of mortgage-backed securities to get to 0, if they were to begin directly selling these assets at a loss due to higher rates making these bonds trade at a discount to par currently, that would be an issue. Instead, one strategy they could do is slow down QT and stretch it out so that they have more time to lower interest rates which would alleviate that unrealized loss on their MBS book. By doing so, this would allow them to get rid of their MBS book without taking the hit. There’s an interesting mirror effect to this exact debate surely happening in commercial banks right now as well who are sitting on large unrealized losses. By lowering rates again, they will be able to close the discount on these bonds and decrease the losses.

This FOMC meeting took a lot of market participants who’ve been too in the weeds on CPI and other single MoM metrics by surprise. It is essential to consider a holistic approach and remember that the Fed is a huge entity that prefers to move slowly and iteratively. If they were to excessively react every month to the latest CPI reading, there would be way too much volatility within the Fed reaction function.

Overall, this FOMC meeting was very dovish and bullish for risk assets:

- We received confirmation that the Fed still plans to cut rates this year. And with no recession on the horizon, these cuts can be considered bullish cuts since the economy remains very strong.

- QT is going to be slowing down and the light at the end of the tunnel is drawing close. On the margin, this will be positive for liquidity.

- The degree to which Powell brushed aside concern around a couple of hot inflation prints humbled many market participants and emphasized how as long as the inflation isn’t high enough to kick in a hawkish reaction, it is extremely positive for risk asset.