As we have entered an era of Fiscal Dominance, the degree to which we run deficits during times of economic expansion, the amount of debt in the financial system, and that higher interest rates make the volatility of fixed income duration higher, understanding the composition and direction of debt issuance from the Treasury has become an increasingly important factor into one’s macro framework.

At the core of this framework lies the Treasury Borrowing Advisory Committee’s QRA, or Quarterly Refunding Announcement report, where a committee lays out the recommendations for how the Treasury should fund the government’s obligations.

During times of increasing government deficits, understanding how the Treasury will fund the gap between its revenues and its obligations is key.

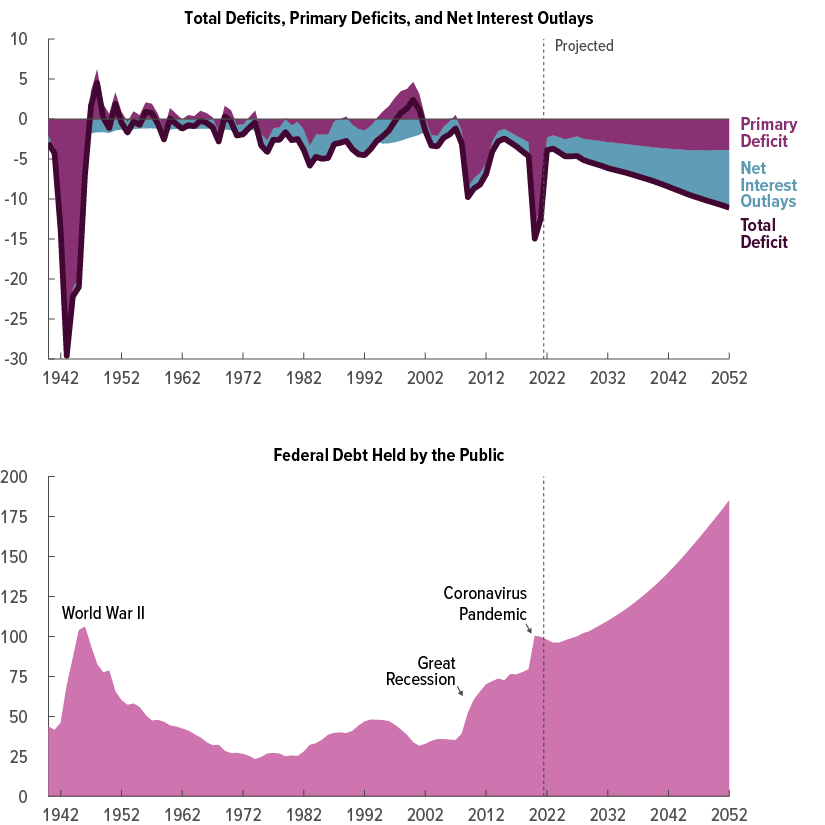

As we have seen in this chart from the Congressional Budget Office, Deficits are expected to increase dramatically over the next decade as a % of GDP largely due to increased interest expenses:

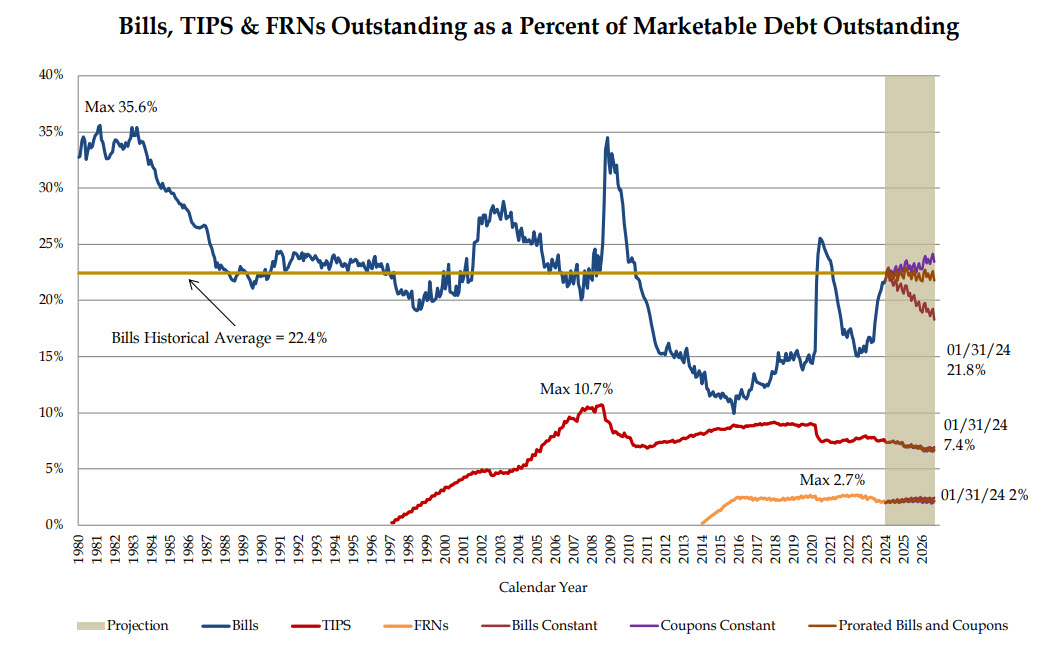

In the last QRA in November, TBAC advised that they would overweight bill issuance to lead to a composition of bills vs other tenors being above its 20% norm.

Looking at Treasuries outstanding, we now see that the Treasury has reached this level of 22% as prescribed.

The vast majority of this bill issuance has been funded by the RRP facility, which has been in a downward trend for the entire quarter:

With that in mind, all eyes are on where issuance is headed for the first quarter of 2024.

Dollar Value:

On Monday, we received an indication that net borrowing for the quarter would be $760b, $55b lower than the estimated $815b from the previous quarter. Therefore, going into Wednesday’s TBAC report, we already knew that the total $ value of debt issuance would be lower than expected. This led to yields heading lower and prices going higher.

Composition of the debt:

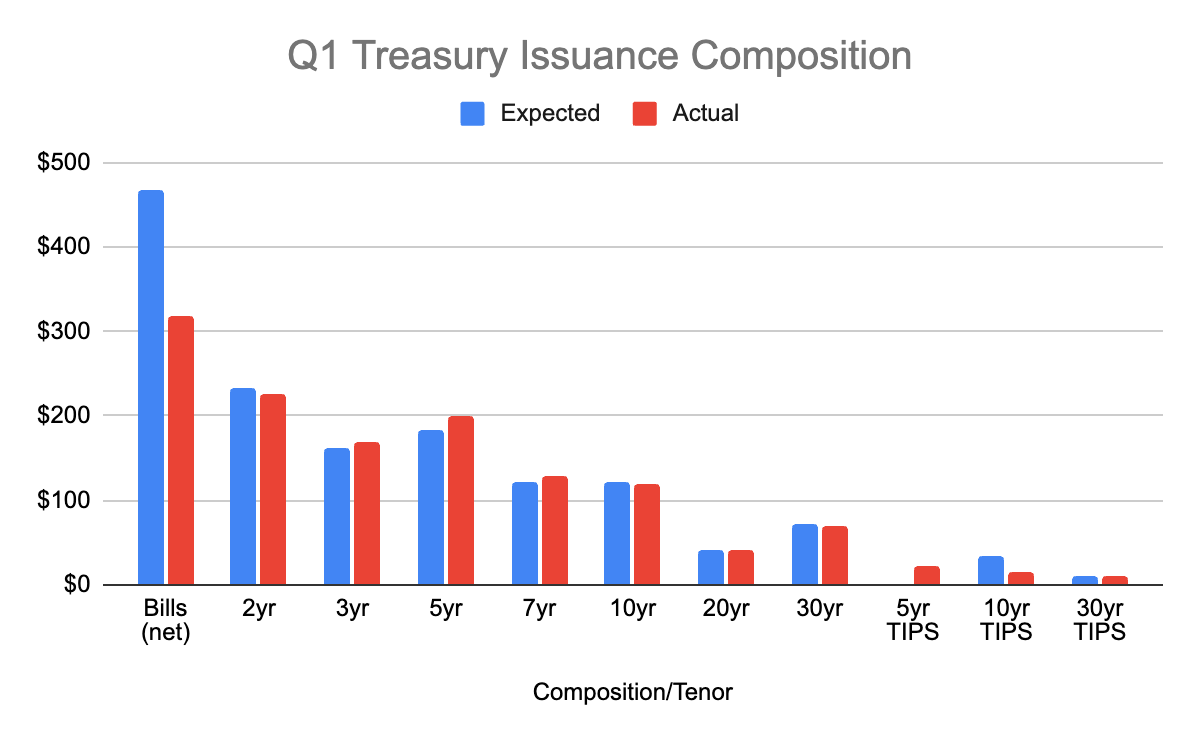

On Wednesday morning, we received the updated composition of the debt for Q1. The following chart compares what was expected in November for the quarter vs what will actually occur:

Key takeaways:

- Overall, there will be an increased % of the composition that will be coupon issuance vs what was expected last quarter, namely from the 5y note going from $183b to $201b.

- Overall net bill issuance is significantly less than expected, decreasing from $468b to $318b

- TIPS issuance will have a generally shorter duration than what was expected

- Little to no change in the long duration bonds 10yr+

- Overall, comparing the estimate to the actual, the key takeaway is that there will be more duration being offered to markets, and less short term T-bills. That said, the change in the amount of duration will be small.

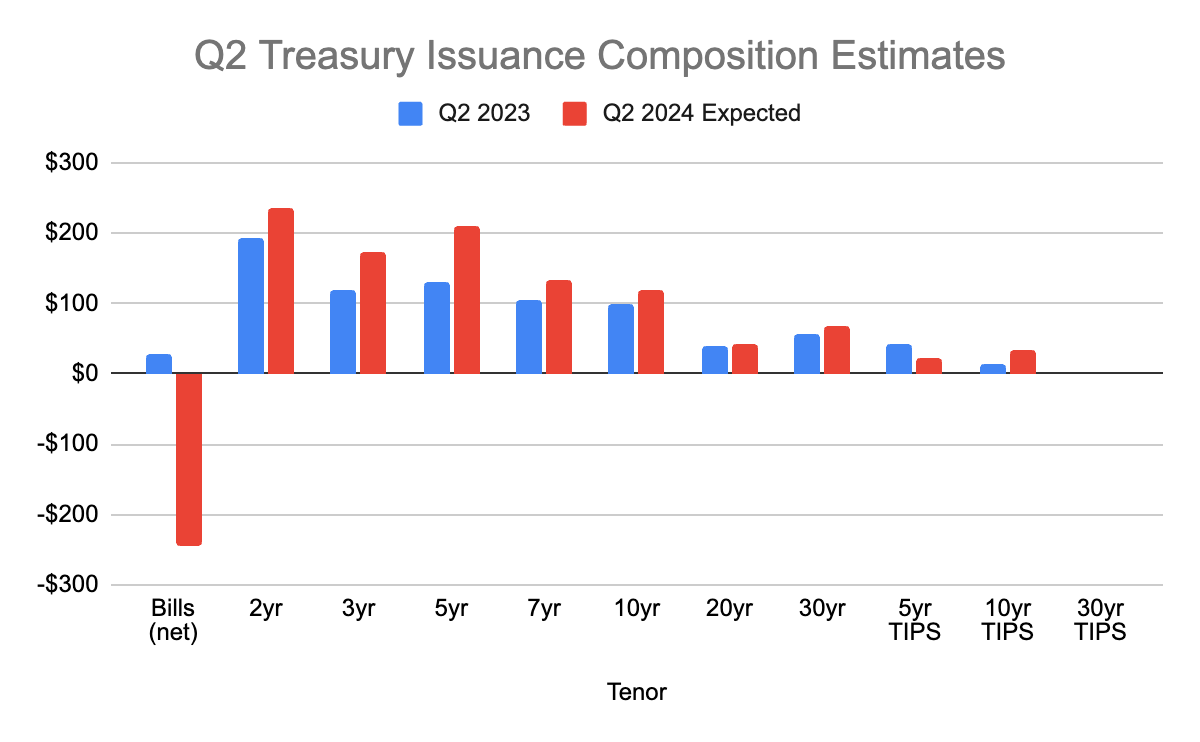

As well, we received Q2 estimates of financing needs from the Treasury. Below is a chart comparing last year’s Q2 actual borrowing to Q2 2024’s estimate of borrowing:

Key Takeaways:

- Unsurprisingly since the deficit the government is running is much larger, the absolute $ value of debt being issued is larger: Total Coupon issuance is $1.037T vs $800b last year.

- The negative net Bill issuance is largely due to higher than expected tax receipts coming in during Q2, as well as a large buffer of existing short term debt that will not be reinvested and will be let to mature off.

- As noted in the TBAC report, the amount of coupon issuance will be neutral and will not increase. Q1 2024 is the last quarter for the foreseeable future where there will be an increase in the % of coupons issued.

Overall, this report paints a picture of the following:

- Less debt issued overall than expected

- Marginally more duration being offered to markets than expected

- Significantly less bill issuance in the next two quarters than recent history

- Continued increase in the amount of interest expenses for the Treasury to pay out to.

In terms of the potential market impacts this may have moving forward, the most significant are the following:

- Due to there being significantly less bill issuance moving forward than recent quarters, the RRP which has been in a major downtrend will most likely flatten out around this $500-600b level.

- The net increase in duration of debt was so minimal that we expect there to be minimal price impact on bonds.

- Since the assumption of QT beginning to end in the spring has been anchored to the idea that RRP will be at 0 soon causing bank reserves to move from an abundant regime to an “ample” regime, the decrease in the amount of bills being issued in the medium term will most likely delay the timing of the beginning of the QT unwind.

- One final mention is in the report TBAC mentioned their plans to begin a Treasury Buyback program in the next quarter. The plan as it stands is for them to do a couple of “test” buys in the next two months, with the goal to fully ramp up the buyback program in the May TBAC report onwards. This will soon become a key facility to understand as the idea is for Yellen to issue T-bills as a means to “buyback” off the run and illiquid longer duration bonds, increasing the liquidity of the Treasury system.

Disclaimer: This research report is exactly that — a research report. It is not intended to serve as financial advice, nor should you blindly assume that any of the information is accurate without confirming through your own research. Bitcoin, cryptocurrencies, and other digital assets are incredibly risky and nothing in this report should be considered an endorsement to buy or sell any asset. Never invest more than you are willing to lose and understand the risk that you are taking. Do your own research. All information in this report is for educational purposes only and should not be the basis for any investment decisions that you make.